Venture debt financing for tech companies: 2026 guide

Most tech founders reach Series A or B with the same quiet fear: every equity round that funds your growth also permanently reduces your ownership. Venture debt financing for a tech company addresses this problem directly. Rather than selling more equity at an inconvenient valuation, you borrow capital against your existing investor backing, contractually committed revenues, or company assets. This guide covers what you need to qualify, how to execute a deal, how to manage the risks, and where founders and CFOs commonly go wrong. It is written for operators who already understand their cap table and want to use debt strategically.

Table of Contents

- Key takeaways

- Prerequisites for venture debt financing

- Executing a venture debt round

- Managing risks and common pitfalls

- Using venture debt to drive growth

- My perspective on venture debt timing and partner selection

- How Meethayat can support your venture debt strategy

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Start preparation early | Allow 6 to 12 months for credit readiness before you actually need the capital. |

| Partner fit over pricing | Choose a lender based on flexibility and relationship quality, not the lowest interest rate. |

| Debt is a growth tool | Use venture debt to extend runway or fund specific initiatives, not to rescue a struggling model. |

| Covenants carry real risk | Loan agreements restrict operational freedom; negotiate terms carefully before signing. |

| Warrants dilute founders | Most venture debt deals include warrants, so model the dilution impact before committing. |

Prerequisites for venture debt financing

Getting venture debt financing right for your tech company starts long before you approach a lender. The preparation phase is where most founders underestimate the work involved.

There is a structural 6 to 12 month gap between deciding to seek venture debt and actually receiving funds. That timeline exists because lenders require audited financials, board-approved budgets, robust reporting systems, and clear evidence of financial discipline. If your finance function is still running on spreadsheets and your last audit was 18 months ago, you are not credit-ready regardless of how strong your revenue growth looks.

Here is what lenders typically assess before offering a term sheet:

- Revenue quality and predictability. Annual recurring revenue (ARR), monthly recurring revenue (MRR) growth rate, churn, and net revenue retention. Lenders want to see revenue that does not evaporate.

- Burn rate and runway. Your current monthly burn and how many months of runway you hold post-financing. Most lenders will not step in when you have fewer than six months remaining.

- Unit economics. Customer acquisition cost (CAC), lifetime value (LTV), and payback period. Venture debt works best for companies with proven unit economics, not those still searching for product-market fit.

- Prior equity rounds. The amount of venture debt tends to be sized at approximately 20% of your last equity raise. A £10 million Series A typically positions you for £1.5 to £2 million in debt.

- Collateral mapping. Detailed collateral mapping against committed recurring revenue or specific assets requires early preparation with your finance team.

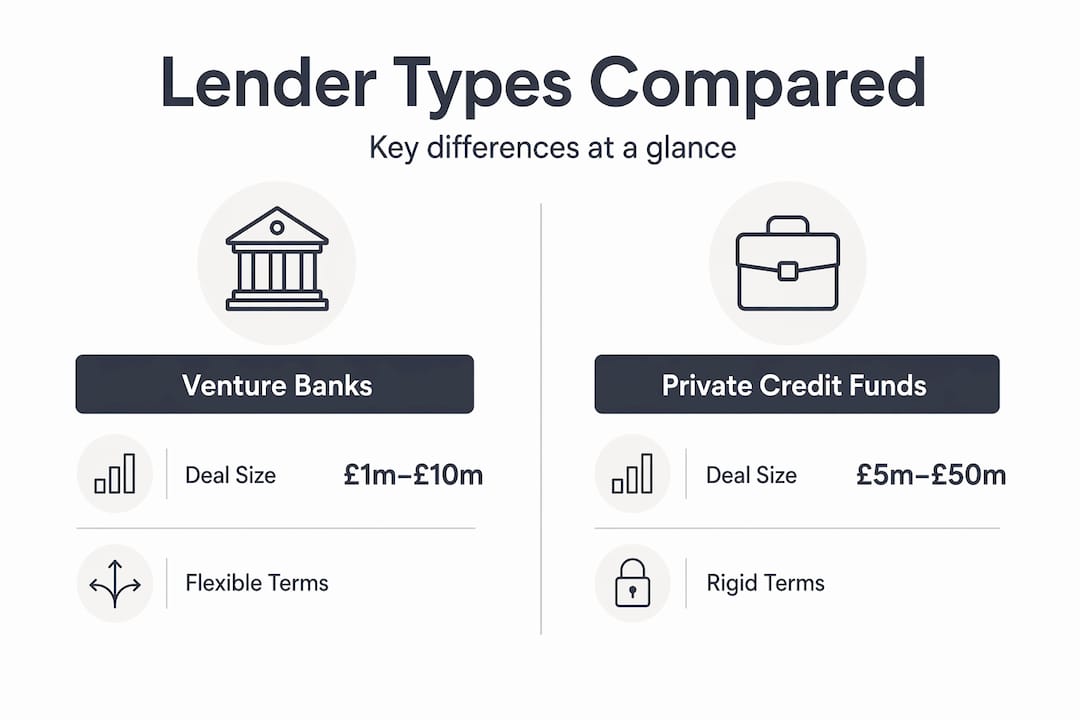

You will also need to understand the type of lender you are approaching. Traditional venture banks offer smaller, more regulated facilities with tighter underwriting criteria. Private credit funds have grown significantly post-SVB and tend to offer larger deal sizes with more bespoke structures. The right choice depends on your growth stage and how much operational flexibility you need.

Pro Tip: Engage a fractional CFO or experienced finance lead at least six months before you intend to raise venture debt. Getting your reporting, forecasting, and collateral documentation in order takes longer than founders expect, and lenders notice the quality of your finance function immediately.

Executing a venture debt round

Once you are credit-ready, the execution process has distinct stages. Moving through them methodically reduces the risk of accepting unfavourable terms or the wrong lending partner.

- Map your lender universe. Identify which lenders are active in your sector, geography, and deal size. The 2026 market includes traditional venture banks and specialist private credit funds. Ask your existing investors which lenders they have worked with previously.

- Run a parallel process. Approach three to five lenders simultaneously. Competition produces better terms and gives you comparative data on pricing, covenants, and warrant structures.

- Analyse term sheets carefully. Do not fixate on the headline interest rate. The terms that matter most are covenant restrictions, warrant coverage, prepayment penalties, draw-down periods, and what triggers a default.

- Negotiate on the right dimensions. Prioritise lending partner fit over the lowest rate. A lender who will work with you through a difficult quarter is more valuable than one who offers 50 basis points less but calls a default at the first covenant miss.

- Conduct legal due diligence. Your lawyer must review the facility agreement, the security package (which assets are pledged), and any warrant agreements before you sign.

- Time it correctly. Venture debt is typically used shortly after an equity round closes, when your balance sheet is strongest and lender confidence is highest.

Comparing lender types

| Dimension | Venture banks | Private credit funds |

|---|---|---|

| Typical deal size | £1m to £10m | £5m to £50m+ |

| Underwriting speed | 8 to 12 weeks | 6 to 10 weeks |

| Covenant rigidity | Higher | More negotiable |

| Warrant expectation | Common | Common |

| Regulatory environment | Heavily regulated | Less regulated |

| Relationship style | Long-term banking | Deal-by-deal |

Pro Tip: Ask every lender how they have handled a portfolio company that missed a covenant in the past 24 months. Their answer tells you more about the relationship you are buying into than any term sheet provision.

Managing risks and common pitfalls

Venture debt is not inherently dangerous. It becomes dangerous when founders do not fully understand what they have agreed to or use it in the wrong context.

The most consequential risk is over-leveraging. If you borrow against optimistic revenue projections and growth stalls, you face a repayment schedule that consumes cash you no longer have. Unlike equity investors, lenders do not absorb downside. They have contractual rights and will exercise them.

Covenants deserve particular attention. Loan agreements routinely include provisions restricting acquisitions, further borrowing, changes in control, and distributions. These restrictions can quietly block strategic decisions months after you have forgotten the terms you signed. Negotiate hard for operational headroom before closing.

Warrants are the second dilution event most founders do not model carefully enough. Venture debt lenders frequently request warrants representing the right to purchase equity at a fixed price. The coverage is typically 1% to 2% of the loan amount as equity, which sounds modest until you calculate it at exit.

Venture debt should function as a strategic accelerant for a business that already works, not as a mechanism to delay the moment when you admit it does not. Using debt to fund a broken model buys time but compounds the damage.

The impact on future fundraising is also underestimated. An upcoming Series B investor will see your debt facility on the balance sheet and factor it into their valuation and terms. If your lender holds a security interest over key assets or IP, that complicates the due diligence process considerably.

Finally, early and regular communication with your lender after closing is not optional. Lenders who are surprised by bad news become adversarial quickly. Lenders who are informed early have both the time and the motivation to find a constructive path forward. Most founders underinvest in this relationship once the money is in the bank.

Using venture debt to drive growth

When deployed correctly, venture debt is one of the most capital-efficient tools available to a scaling tech company. The core use case is extending your cash runway by six to twelve months. Venture debt extends runway and bridges valuation inflection points without the equity dilution that comes from raising a new round at a suboptimal moment.

Consider a SaaS company post-Series A with £8 million in the bank and 18 months of runway. With £1.5 million in venture debt, that same company gains an additional four to six months of runway at current burn rates, enough time to hit the ARR milestone that justifies a higher Series B valuation. The equity you preserve by waiting for that milestone is worth materially more than the interest cost of the debt facility.

Strategic use cases for venture debt

| Use case | What debt funds | Why debt is preferable to equity |

|---|---|---|

| Market expansion | Sales hiring, new geography costs | Avoids dilution before revenue confirms market fit |

| Product development | Engineering resource for a defined feature set | Short payback period makes debt economics work |

| Tuck-in acquisitions | Purchase price for small bolt-on targets | Acquisition assets often provide collateral |

| Working capital | Bridging gap between SaaS invoicing and collections | Temporary, self-liquidating need |

| Runway extension | General operating costs between rounds | Buys time for valuation growth without equity cost |

The KPIs to monitor after closing a venture debt facility include monthly debt service coverage ratio (DSCR), ARR growth trajectory relative to projections used in underwriting, covenant headroom on each financial maintenance test, and warrant dilution as a percentage of fully diluted share count. Build these into your monthly board reporting from day one.

Pro Tip: Model three scenarios before committing to a venture debt facility: base case, downside, and severe downside. If the debt repayment schedule is survivable in your severe downside scenario, the facility is sized correctly. If it is not, renegotiate the tranche structure before signing.

Founders exploring advisory support for tech startup funding strategies should treat venture debt as one instrument within a broader capital structure, not the entire strategy. It works in concert with equity, not as a replacement for it.

My perspective on venture debt timing and partner selection

I have sat on the CFO side of three exits, and venture debt has featured in two of them. Here is what I have found that most guides do not say plainly.

The conventional advice to minimise your interest rate is genuinely misleading. When I have seen founders optimise for the lowest rate, they have often ended up with lenders who have rigid covenant structures and no appetite for a constructive conversation when the business goes through a rough quarter. The 50 basis points they saved became irrelevant when they needed a waiver and got a formal letter of default instead.

The lenders who prioritise founders’ trustworthiness and execution capability over purely financial metrics are the ones worth working with. That quality is identifiable before you sign. Ask them about the worst deal they have had in the past three years and how they managed it. Ask what their internal process is when a company misses a covenant. The answers are diagnostic.

What I have also learned is that venture debt is a tool for a working machine, not a rescue mechanism. Every time I have seen it used to extend runway for a company with a fundamentally broken growth model, it has ended badly. Not just for the founders, but for the employees who deserved a faster, cleaner decision about the business’s future.

My practical advice: raise venture debt when you do not desperately need it. The best time to borrow is when your metrics are strong, your equity round just closed, and you have options. That is when you negotiate from strength. Waiting until you are six months from zero means you will accept whatever terms the lender offers, and they will know it.

, Hayat

How Meethayat can support your venture debt strategy

Preparing for and managing a venture debt facility is not just a financial exercise. It requires precise documentation, disciplined forecasting, and ongoing covenant monitoring that most early-stage finance teams are not resourced to handle on their own.

Meethayat offers fractional CFO services tailored to tech founders and CFOs navigating exactly this process. From building the financial models and collateral packages that lenders require, through negotiating term sheet provisions, to setting up the post-close reporting systems that keep you compliant, Hayat Amin brings three exits of practical CFO experience to your financing strategy. If you are planning a venture debt raise in the next 12 months, the preparation work starts now. You can also explore guidance on how to hire a startup advisor to find the right support structure for your stage and goals.

FAQ

What is venture debt and how does it differ from equity?

Venture debt is a loan product for venture-backed companies that provides capital without immediate equity dilution. Unlike equity, it must be repaid with interest and often includes warrants, but it preserves ownership for founders at critical growth stages.

When is the right time to raise venture debt?

The optimal timing is shortly after closing an equity round, when your balance sheet is at its strongest and your metrics are most compelling. Venture debt raised post-equity round typically attracts better terms and more lender interest.

How much venture debt can a tech startup access?

Venture debt is typically sized at around 20% of the last equity raise. A company that raised £10 million in Series A can generally access £1.5 to £2 million in venture debt, subject to lender assessment of financial health.

What are the main risks of venture debt for tech companies?

The primary risks are covenant restrictions limiting operational flexibility, warrant dilution, over-leveraging against optimistic projections, and the contractual obligation to repay regardless of business performance. Covenants restrict company actions and must be negotiated carefully before signing.

Do I need audited financials to qualify for venture debt?

Yes. Most lenders require audited financial statements as part of the credit assessment process. The 6 to 12 month lead time for securing venture debt reflects how long it takes to get these prerequisites in order if they are not already current.