Tech company M&A financial prep: 2026 guide

Getting tech company M&A financial prep right is the single biggest lever separating deals that create shareholder value from those that destroy it. Over half of tech M&A deals fail to generate significant shareholder value within two years, and the root cause is rarely the deal price. It is almost always inadequate financial preparation and poor integration execution. This guide covers the critical workstreams every CFO must own before signing: financial documentation, synergy modelling, regulatory filings, and emerging AI diligence obligations.

Table of Contents

- Key takeaways

- Financial documentation for M&A due diligence

- Synergy modelling and pressure testing assumptions

- Compliance and regulatory financial preparation

- AI diligence and operational financial risk

- My perspective on financial prep that actually works

- Work with Meethayat on your M&A financial preparation

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Documentation drives confidence | Organised, audited financials and recurring revenue metrics instil buyer confidence and accelerate due diligence timelines. |

| Synergy models must be executable | Linking every financial assumption to a specific integration plan separates defensible models from aspirational spreadsheets. |

| Regulatory timing is a CFO responsibility | HSR filing quality and early SEC disclosure alignment directly affect whether a deal closes on schedule. |

| AI governance gaps create warranty risk | Undocumented AI validation procedures can jeopardise representations and warranties and increase transaction risk. |

| Integration execution beats financial modelling | The CFO’s role does not end at signing. Post-merger execution determines whether synergies actually land. |

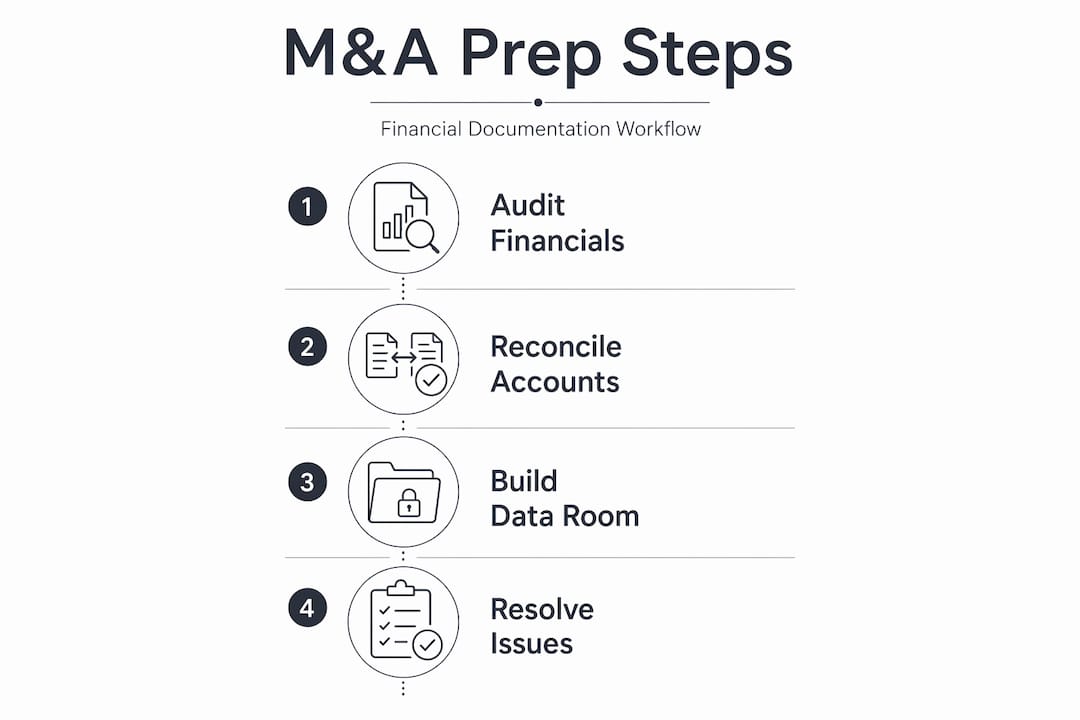

Financial documentation for M&A due diligence

The data room is where deals are won or lost before negotiations even intensify. Buyers and their advisors will form a view of your business quality within the first 48 hours of diligence access, and what they find in those initial hours shapes every subsequent conversation on price and terms.

Due diligence typically runs 6 to 12 weeks post-letter of intent, and disorganised or incomplete documentation is one of the most cited deal-kill issues. The foundational package should include three years of audited financial statements, interim management accounts, accounts receivable ageing schedules, debt and capital lease schedules, and a detailed working capital analysis showing seasonality and normalisation adjustments.

For tech companies, the financial diligence pack must go further than standard documentation. Buyers will scrutinise revenue quality intensely, particularly in software businesses. SaaS represented approximately 58% of software M&A activity in 2025, and acquirers are pricing deals on recurring revenue durability and margin expansion potential. You need to prepare:

- A normalised EBITDA bridge showing one-off adjustments with clear supporting evidence

- Monthly recurring revenue (MRR) and annual recurring revenue (ARR) roll-forwards by cohort

- Net revenue retention (NRR) and gross revenue retention (GRR) waterfall schedules

- Customer concentration analysis with contractual renewal terms

- Deferred revenue schedules and revenue recognition policy documentation (particularly for ASC 606 or IFRS 15 compliance)

| Document | Preparation tip |

|---|---|

| Audited financials (3 years) | Reconcile to management accounts; resolve any audit qualifications before data room opens |

| Normalised EBITDA bridge | Label each add-back clearly; attach board minutes or contracts as evidence |

| ARR / MRR cohort roll-forwards | Break out new business, expansion, contraction, and churn separately |

| Working capital analysis | Show trailing 12-month averages and seasonal peaks; define your working capital target precisely |

| Debt and equity schedule | Include all convertible instruments, warrants, and employee equity obligations |

Pro Tip: Start building your data room at least 90 days before you expect to receive a letter of intent. Retroactive document gathering under deal pressure introduces errors and signals poor financial governance to buyers.

You can use a free M&A checklist to structure your diligence workstream across finance, legal, and commercial tracks, which helps co-ordinate the CFO’s team with external counsel without gaps.

Synergy modelling and pressure testing assumptions

The most common valuation inflation point in technology mergers and acquisitions is the revenue synergy estimate. Revenue synergies are harder to realise, take longer to materialise, and depend on factors outside the CFO’s direct control. Cost synergies, by contrast, are more predictable, faster to execute, and considerably more credible in a buyer’s model.

BCG research identifies that top-quartile deals achieving around 26% relative total shareholder return do so by linking synergy estimates to specific integration decisions and measurable milestones rather than treating them as pro forma adjustments. The discipline required is mapping every synergy line item to an owner, a date, and a dependency.

The practical framework for defensible synergy modelling looks like this:

- Cost synergies: Identify headcount redundancies by function, vendor contract renegotiations with specific renewal dates, and infrastructure consolidation with migration timelines.

- Revenue synergies: Require a go-to-market (GTM) operating model showing which sales team sells what product to whom, with quota assumptions and ramp periods.

- Dis-synergies: Model customer attrition from brand change, product rationalisation, and key talent departure. Ignoring dis-synergies is the single most credibility-destroying omission in a synergy model.

| Approach | Success factors | Common failure points |

|---|---|---|

| Bottom-up cost synergies | Tied to specific headcount decisions and vendor contracts | Incomplete view of shared service dependencies |

| Revenue cross-sell model | Named customer targets with quota and ramp plan | Assumes existing sales team capacity without enablement investment |

| Infrastructure consolidation | Architecture review complete pre-close | Underestimated migration cost and timeline |

| Product roadmap alignment | Clear decision on product rationalisation pre-day-one | Roadmap decisions deferred, creating customer uncertainty |

Pro Tip: Involve your integration management office (IMO) during the synergy modelling phase, not after signing. Early IMO planning before day one is what separates executed synergies from aspirational slides.

The CFO’s job is to pressure test assumptions against operational reality. If the revenue synergy model assumes cross-selling a new product into an existing customer base, the model needs a signed-off sales enablement plan, not just a TAM slide. Every number in the model should have an owner who agrees to be accountable for delivery.

Compliance and regulatory financial preparation

Regulatory preparation is where tech CFOs are most likely to underestimate time and resource requirements. The consequences of underestimating are severe. A poorly prepared HSR (Hart-Scott-Rodino) filing or an SEC S-4 registration statement with MD&A gaps can add months to a deal timeline and, in some cases, reshape the deal entirely.

The standard HSR waiting period is 30 calendar days, but the quality of the filing determines whether regulators accept it cleanly or issue a Second Request. A Second Request can extend review by 6 to 18 months and requires production of internal documents, financial models, and competitive analyses. The CFO must own the financial narrative in the filing, including forward-looking financial projections that are consistent with board-approved plans.

For SEC-registered deals, S-4 filings attract concentrated SEC comment activity around three specific areas: pro forma financial statement completeness, purchase price allocation methodology, and integration cost classification. The most common comment triggers are:

- Insufficient quantification of acquisition-related costs in MD&A

- Pro forma adjustments that do not reconcile clearly to the announced synergy model

- Goodwill allocation presented without adequate segment-level disclosure

- Integration costs classified inconsistently across restructuring, transaction expenses, and capital expenditure

The strategic remedy is to build a crosswalk document early. Synergy models and disclosure narratives must be synchronised from the moment you begin drafting, not reconciled after the SEC responds. Accounting classifications for integration costs need to be decided before the S-4 is filed, with consistent treatment applied across the pro forma statements, MD&A, and footnote disclosures.

Pro Tip: Assign one person, ideally inside the CFO’s office, to own the crosswalk between the synergy model, the pro forma financials, and the MD&A narrative. Misalignment between these three documents is the primary driver of SEC comment cycles that delay deal timing.

AI diligence and operational financial risk

AI governance has become a material diligence workstream in technology mergers and acquisitions, and most CFOs are not yet treating it with the same rigour as financial controls. AI diligence is primarily a governance exercise, not a technical one. The question buyers are asking is not what AI systems you use. It is whether you can demonstrate that those systems operate within documented, validated governance procedures.

The specific risk category driving this scrutiny is shadow AI: employees using AI tools that are not formally approved, monitored, or documented by the organisation. Where shadow AI has been used in financial forecasting, customer communications, or regulatory reporting, it creates gaps between your representations and the operational reality that warranties are meant to cover. Lack of evidence trails can jeopardise warranties and materially increase transaction risk.

Your financial diligence pack for AI risk areas should include:

- A register of AI tools used across finance, legal, sales, and operations, with approval status and governance documentation for each

- Validation procedures for any AI outputs used in financial reporting or forecasting

- Evidence that AI-generated analysis has been reviewed and approved by qualified personnel before being relied upon

- Warranty language that is mapped to operational reality, with evidence trails sufficient to support each representation

Pro Tip: Run an internal AI tool audit at least six months before a planned transaction. Discovering undocumented AI use during buyer diligence is significantly harder to manage than addressing it proactively in your own preparation.

This is also an area where enterprise AI agent operations can create documented, auditable workflows that serve as evidence of governance, rather than creating additional risk exposure.

My perspective on financial prep that actually works

I have been through this process three times as a CFO. What I have learned is that the financial model is not the hard part. The hard part is the translation from model to execution.

In my experience, the CFOs who get the best outcomes are not the ones with the most detailed spreadsheets. They are the ones who have had the uncomfortable conversations with the heads of sales, engineering, and HR before the deal is announced. They know which synergy assumptions are real and which ones were inserted to make the IRR work. They are not surprised at month six when the cross-sell revenue is not materialising, because they built the GTM operating model themselves, rather than accepting a deck from the corporate development team.

The contrarian view I hold on technology mergers and acquisitions is this: cultural integration and financial integration are not separate tracks. When the sales team does not understand the combined product suite, the revenue synergy model fails. When IT refuses to consolidate on a shared ERP because of political resistance, the cost synergy model fails. The CFO who treats financial preparation as purely a numbers exercise will be defending miss after miss in the first post-merger board meeting.

My practical advice is to hold a synergy assumption review with each functional owner before the deal is signed. Force every assumption back to a named person, a date, and a documented plan. That process alone will eliminate the aspirational 30% of the synergy model that no one actually believes, and it will make the remaining 70% genuinely executable.

, Hayat

Work with Meethayat on your M&A financial preparation

Executing tech company M&A financial prep at a standard that holds up under buyer scrutiny and regulatory review requires both financial precision and operational awareness. Meethayat offers two services directly relevant to this challenge.

The AI agent operator service deploys agents that automate document management, data verification, and workflow co-ordination across your diligence workstreams. This includes structured data room population, recurring revenue metric extraction, and audit trail documentation for AI governance requirements. The fractional CFO service brings three-times-exited CFO experience to your transaction, covering synergy modelling, SEC disclosure alignment, and post-merger integration execution. Whether you are preparing for your first acquisition or managing a complex cross-border deal, Meethayat delivers the depth that SaaS-focused financial leadership requires. Contact Meethayat to discuss your upcoming transaction.

FAQ

What documents are needed for tech M&A due diligence?

The core financial package includes three years of audited financials, interim management accounts, normalised EBITDA bridges, ARR and MRR roll-forwards, working capital analyses, and debt schedules. SaaS businesses should also prepare NRR and GRR waterfall schedules and revenue recognition policy documentation.

How long does tech M&A due diligence take?

Due diligence typically runs 6 to 12 weeks following the letter of intent. Disorganised documentation or incomplete financial records are among the most common causes of delays and deal-kill issues.

How does HSR filing quality affect deal timing?

The standard HSR waiting period is 30 days, but a poorly prepared filing can trigger a Second Request, extending review by 6 to 18 months. CFOs must own the financial narrative in the filing and ensure forward-looking projections are consistent with board-approved plans.

What triggers SEC comment letters in M&A filings?

SEC comments on S-4 filings most commonly target insufficient MD&A quantification of integration costs, pro forma adjustments that do not reconcile to the synergy model, and inconsistent accounting classifications across disclosure documents.

Why does AI governance matter in tech M&A diligence?

AI diligence is a governance exercise focused on whether AI tools are documented, validated, and operating within approved procedures. Shadow AI use without evidence trails can expose gaps between representations and operational reality, increasing warranty risk for sellers.